Now that you have calculated your tax liability for this year, you will know exactly how much you have to save to minimise your tax outgo. You have two choices. If you are short of liquid surplus funds to invest, you can simply go ahead and pay this tax.

Outlook Money strongly recommends that you do not take a personal loan or any other debt to pay off this tax liability. If you have surplus funds and are ready to part with them for a medium- to long-term period (about five years or more), you can choose option two and invest them in the specified Section 80C instruments. The amount you invest will be reduced, up to Rs 1 lakh, from your gross total income.

Apart from long-term savings, the underlying objective of investing in any of the Section 80C instruments is to save your taxes.

Tax is paid on the income left after the amount invested is deducted from the gross total income. Taking an example, investment of the maximum allowed amount of Rs 1 lakh in one or a mix of Section 80C instruments reduces the taxable income by Rs 30,900 and Rs 33,900 if the income tax rate is 30.9 per cent and 33.99 per cent, respectively.

However, the days of merely looking at the tax benefits of tax-saving investments are over. Now, you can, based on your risk profile, choose to invest in products that save tax as well as earn returns.

The Income Tax Act does not treat 80C instruments uniformly, and the taxability of contributions, accumulations and withdrawals differs from one instrument to another.

Investments in a public provident fund (PPF) scheme, for instance, enjoy tax relief in the form of deductions, while the interest escapes the taxman's axe. The money you get on maturity is not taxable either.

This method of taxation is referred to as 'exempt-exempt-exempt' (EEE) since all three stages -- contribution, accumulation and withdrawal -- are exempt from tax.

On the other hand, contributions to and accumulations in certain products are not taxable, but the amounts received, like periodical pension in a pension plan, are taxable in the year of receipt. Such financial products are governed by the 'exempt-exempt-tax' (EEE) method of taxation.

The tax treatment is different for notified tax saving bank fixed deposits (FD), National Savings Certificates (NSC) and Senior Citizens Savings Scheme (SCSS). The investment made in these instruments qualifies for exemption at the time of contribution, but the interest earned is taxed on accrual basis, that is, on each-year basis.

For example, if a notified tax saving bank FD gives a return of 8 per cent per annum, the effective post-tax return would be a mere 5.5 per cent, lower than the inflation rate, for someone paying 30.9 per cent tax. On the other hand, PPF gives a tax-free return of 8 per cent per annum. This return is the same for all tax brackets.

The return that should be examined while comparing tax saving products is the one post-tax, not pre-tax. The returns of tax-free products like and employees' (EPF) are not pruned by taxes. With the tax scissors not clipping it, PPF's return stays at 8 per cent per annum for all tax brackets.

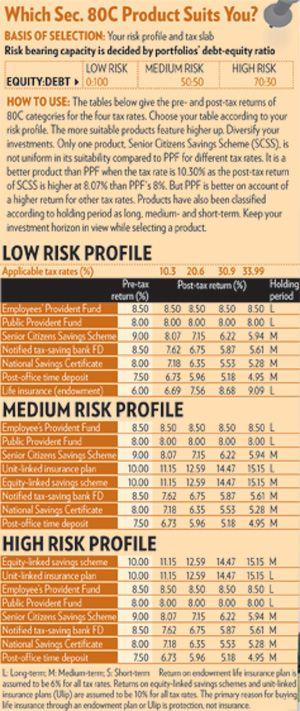

We have shown the relative suitability of different 80C products on the basis of their returns for the four tax rates

The relative performance of only one product, SCSS, is not uniform across different tax rates. SCSS scores over in the 10.30 per cent tax bracket as the post-tax return of SCSS is higher at 8.07 per cent than 8 per cent. But beats SCSS on the return parameter for other tax rates. However, that would again change if the senior citizen's income is less than the minimum taxable amount of Rs 2.25 lakh a year.

Other than the post-tax return, your choice largely hinges on your perception of the risk involved, your financial background and the stage of life you are in. Many young individuals are reluctant to invest in equity-related instruments at the initial stages of their career.

At the other end of this spectrum are investors in their late fifties or even retired people who have embraced the equity culture. Equity had moved unilaterally in the last five years, but we saw a reversal this year. cannot be relied on as an asset class to give good positive returns in the short- to medium-term.

So, while retirees may have had nothing to complain about till January 2008, the story is completely different for people who have retired since.

The question then is: What comprises a portfolio that can stand the test of time and deliver a decent return over a long term?

Too much exposure to equity may skew the risk-reward ratio. A bias towards fixed income instruments, on the other hand, may adversely impact the post-tax and post-inflation return. Risk and return have a close relationship and are important pillars of wealth creation over the long term.

Linking your 80C investments to your long-term financial goals is a recognition of this fact. Liquidity is a crucial factor in all the instruments and, hence, short- and long-term objectives should be clear before you lock your funds in them.

Remember, there is a trade-off in the choice between a market-linked product and an assured return instrument that is not linked to market conditions. The liquidity, returns and safety of your funds should be an integral part of your investment decision.

Hence, it is essential to have a portfolio with a prudent mix of market and non-market products. A portfolio that has an unreasonable bias towards any one of the two categories needs corrective action.

And, therefore, the final choice of instrument categories should, ideally, be based on a combination of factors rather than solely being driven by returns. One instrument by itself cannot help you save tax and provide safe, assured and high return at the same time.

The endeavour should be to build a portfolio that can deliver a decent return with little risk.

The product categories are stacked as per their post-tax return in the adjacent table. Essentially, this gives you an idea which class would be more suitable to you in terms of the actual return in your hand.

The choice of the instrument would further hinge on your risk appetite. The table details three risk profiles: low, medium and high. Under each investor risk category, the products are stacked as per their return and risk profile.

Taxpayers in the low risk category can, for instance, continue their EPF account and then consider any of the products shown. Being averse to risk, it would be better for them to avoid products that invest in equity, such as equity-linked savings schemes (ELSS) and unit-linked insurance plans (Ulips).

Endowment plans would be the best way to take life cover for them. However, taxpayers in the medium-risk category may benefit if they replace life insurance endowment plans with Ulips or ELSS.

Having both an endowment plan and a Ulip would amount to duplication of benefits as both serve the basic objective of providing protection. Investors in the high-risk category should give priority to equity-linked products such as ELSS or Ulips over fixed income products.

Once you have identified products that suit your risk profile, do also consider their holding period. funds diverted towards tax-saving instruments need to be locked in for at least three years, in many cases more. Some products have a lock-in mandate and they should never get money that you feel you are likely to require in this period.

A good mix of medium- and long-term products should be present in your portfolio to help you not just save tax but also fulfil your financial objectives.

Wealth can be created over the long tem only from a decent real rate of return, that is, after taking inflation into account.

Finally, having made your investments and claimed the tax breaks, don't forget to keep the records and documents of your investments and tax deduction certificates, since you will have to produce them if called upon to do so by the taxman.